What NCFX 24x7 FX-from-Crypto Data Reveals About Market Structure

- Feb 26

- 3 min read

With data now flowing from our new 24x7 FX from crypto feed we are starting to build a picture of how the two markets relate to each other. We wanted to share some initial findings.

We use the same methodology to create all our fiat from crypto currency pairs. For the most liquid pairs, we find that during the periods when both fiat and crypto markets are open, they move broadly together (more on that later). This gives us confidence that the methodology we use to extract the fiat rate from the crypto markets is sound. In less liquid markets differences between 24x7 and fiat tell us something about the structures of those markets.

Our initial findings suggest that this "basis"—the delta between traditional fiat rates and crypto-derived rates — is a signal of market maturity and regulatory constraint.

The Alignment of Liquid Markets

In high-liquidity environments, specifically the G10 currency pairs, the correlation between traditional fiat and crypto-derived rates is remarkably tight. Our analysis of the EURUSD pair (see Chart 1) confirms that when both markets are active, they move in near lockstep.

Interestingly, we observed a slight temporal lead in traditional fiat markets. This "lag" in the crypto space is a logical byproduct of current liquidity concentrations; flow-driven price discovery still originates in the deeper, institutionalised FX markets. This alignment validates that our methodology for extracting fiat rates from crypto markets is fundamentally sound.

Structural Friction: The Case of the Yen and Restricted Pairs

While most G10 pairs show parity, the Japanese Yen (JPY) presents a compelling anomaly. Despite high cointegration, the USD consistently trades at a small but significant premium in the crypto-derived market (see Chart 2).

This premium mirrors what we see in restricted currency pairs, albeit without the overt regulatory hurdles. We attribute this to crypto-specific infrastructure constraints: there are currently fewer efficient on-ramps through stable coins for USDJPY than for its G10 peers. This highlights a critical utility of our data: it serves as a real-time gauge for the development of liquidity and "plumbing" within the crypto ecosystem itself.

The Information Value of the "Basis"

In markets where significant Non-Deliverable Forward (NDF) activity exists, the basis widens. Here, the USD often trades at a substantial premium in crypto markets—a reflection of the inherent demand for dollar outflows in regions where traditional currency controls are stringent. The example below in Chart 3 shows USDBRL.

From a statistical perspective, the distribution of this basis is telling:

Normalisation: For most pairs, the basis follows a normal distribution.

Excess kurtosis: While some pairs exhibit "fat tails" (outliers), we expect these to diminish as crypto market depth evolves.

Predictive power: By understanding the specific mean and standard deviation of a pair’s basis, managers can use crypto market movements during weekend "blackout" periods to predict fiat opening rates with increasing accuracy.

Weekend Volatility and the Signal-to-Noise Ratio

One of the most reassuring findings involves weekend trading. One might expect volatility to spike during the fiat market's "off-hours" due to lower liquidity. On the contrary, we found that volatility actually decreases during the weekend.

This suggests a high signal-to-noise ratio. In the absence of economic releases, corporate hedging, or company updates, the crypto-derived fiat feed remains stable, reflecting a market that is not merely "noise," but a rational extension of the global financial system.

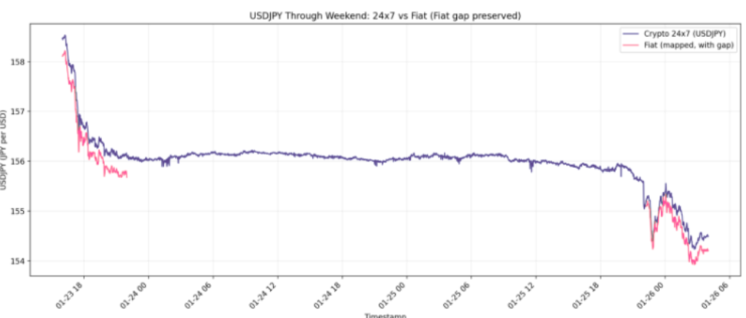

In Chart 4 below we can see the USDJPY rate formed in the fiat market and the 24/7 fiat from crypto rate across a weekend. You can see how the fiat market closes and opens and how the crypto market continues across the weekend and how its path perhaps gives some queues to where the fiat market will open and how it might behave as liquidity is forming. Of course, an alpha model would need robust testing and validation, but the potential seems clear.

Strategic Implications

The value of this data lies not in seeing the same price in two places, but in understanding why they differ. As our dataset deepens, we see three primary use cases for market participants:

Arbitrage and risk management: Quantifying the cost of liquidity across different market structures.

Predictive modelling: Leveraging 24x7 crypto signals to anticipate traditional market gaps.

Structural analysis: Monitoring the health and maturation of crypto-on-ramps via basis compression.

We are just beginning to scratch the surface of what this cointegrated view of the world’s currencies can tell us about the future of global liquidity. As the data begins to be distributed to our partners and clients, we expect the benefits of the important insight it affords to be quickly exploited.

Comments